The silliest way to save $4 per week, part 1

A story about a Subway puzzle.

Dorsey's devilish desire

The first piece of this puzzle came to my attention when a friend clued me in to Cash App's MTA boost. Cash App is a service for sending people money. You can also get a debit card through Cash App and, to get people to use the card, they offer a variety of discounts called boosts. One of these boosts is (at writing time, the terms seem to change somewhat frequently) $1 off any purchase of more than $1 from the MTA every six hours. The MTA (Metropolitan Transit Authority) runs the subway, so this means you can get $1 off of a subway ride every six hours. Subway rides are normally $2.75, so you can ride the subway for $1.75 every six hours. You can also ride for 13 cents if you're particularly dedicated, but I don't think it's practical so let’s never talk about that again.

Riding the subway for $1.75 is great. It's like taking a time machine to the early 2000s. I ride the subway almost every day, multiple times a day, so you can imagine how excited I was to hear about this. I signed up for a Cash App card on the spot. There is a little wrinkle though: I already don't pay $2.75 per ride.

The predicament

Arielle just started a new job, and the new job offers a Commuter Benefits card. My job offers one too. A Commuter Benefits card is a debit card one can fill up each month with pre-tax money, which can only be spent on transit. Because the money one puts on a Commuter Benefits card is untaxed, every purchase one makes with it is essentially discounted by one's marginal tax rate. Arielle’s question was this: when should I use the Cash App boost and when should I use my Commuter Benefits card?

Aside: what is a "marginal tax rate?"

Taxes can be complicated, but understanding the idea of a marginal tax rate is critical for understanding the Cash App vs Commuter Benefits problem. In the United States (and most other countries, I think), there is a progressive income tax. Let's make up a person, Bert, and look at a simplified illustration of Bert's federal income tax to get a handle on it.

Money that Bert earns in the U.S. is taxed throughout the year, and they file their taxes at the beginning of the next year to correct any overpayment or underpayment. This is a tax on Bert's income: income tax.

Bert is taxed at a certain rate. Usually, we express income tax rates as percentages. If Bert's tax rate is 20%, that means that for every dollar they earn, they pay 20 cents in income tax. The more money Bert earns, the higher their tax rate. The system is designed such that people who earn more pay a larger portion of their income (because of the marginal utility of money). The portion of Bert's income which is taxed gets progressively larger as their income gets larger: progressive tax.

The way this progression is implemented is through tax brackets. Tax brackets determine the tax rate for income within a range of dollar amounts. Here are the 2022 federal income tax brackets for people filing alone:

So how does Bert use this table to figure out their tax rate for the year? Let's say that Bert makes $100,000 in 2022. The most obvious way for Bert to use the table would be to look for the range that includes $100,000, which is $89,076 to $170,050, and conclude that their tax rate for 2022 is 24%. That is (unfortunately, because it is so intuitive) not correct.

Instead, tax brackets work like buckets that you fill up with your income. Here is an illustration of that for Bert’s 2022:

- Bert first fills up the $0 to $10,275 bucket, paying 10% or $1,027.50 in income tax on this money

- Bert then fills up the $10,276 to $41,775 bucket, paying 12% or $3,779.88 in income tax on this money

- Bert then fills up the $41,776 to $89,075 bucket, paying 22% or $10,405.78 in income tax on this money

- Bert then pours the rest of their income into the $89,076 to $170,050 bucket, paying 24% or $2,621.76 in income tax on this money

Altogether, Bert's tax rate for the year is around 18% instead of 24%. That's a big difference! This bucket-filling system also makes it so that you can never take home less money when a raise pushes you into a higher tax bracket. It is possible to take home less money after a raise due to a benefits cliff, which is horrible and should be fixed, but it is not possible due to taxes.

If Bert earned $10 more in 2022, what would they pay in federal income tax on that $10? Well, there's still room in the 24% bucket, so that's where the new $10 would go and Bert would pay $2.40. That bucket that additional dollars go into is called Bert's marginal tax bracket and the rate that goes along with that bracket is called Bert's marginal tax rate.

Marginal tax rate is what we're concerned about in the Cash App vs Commuter Benefits problem, because putting money on the Commuter Benefits card essentially reduces your taxable income, taking dollars out of that last bucket.

Back to the predicament

Let’s look at this question from the perspective of the median resident of NYC. The Cash App discount of $1 from $2.75 is ~36.4%. According to the 2020 census, the median per capita income in NYC was $41,625. The marginal federal income tax rate on that income is 12%, but in NYC there is state and city income tax too. The 2022 New York State marginal income tax rate at $41,625 is 5.97%. The 2022 New York City marginal income tax rate at $41,625 is 3.819%. All together the median New Yorker’s marginal tax rate for 2022 is 21.789%.

In this example, the Cash App discount is about 36.4%, while the Commuter Benefits discount is about 22.8%, so our commuter saves a significant chunk of change by using the Cash App card! But what about if they need to use the subway two (or more) times within six hours? The Commuter Benefits discount is better than getting no discount, so the intuitive thing would be to pay with the Cash App card when the boost is available, and with the Commuter Benefits card when the boost isn't available. Unfortunately, there's another complication.

OMNY

The MTA began rolling out a more modern payment method, OMNY, in 2019, and by December 2020 it was available on every bus and at every subway station in NYC. Metrocards are going the way of the subway token.

With OMNY, when you ride the subway twelve times in a week using a given credit or debit card, all future rides on that card are free for the rest of the week. This throws a wrench in the use-Cash-App-when-boosted-and-Commuter-Benefits-card-otherwise plan. Using the Cash App card unboosted costs more than using the Commuter Benefits card, but free rides are better than any discount and using the same card every time brings free rides faster than mixing cards.

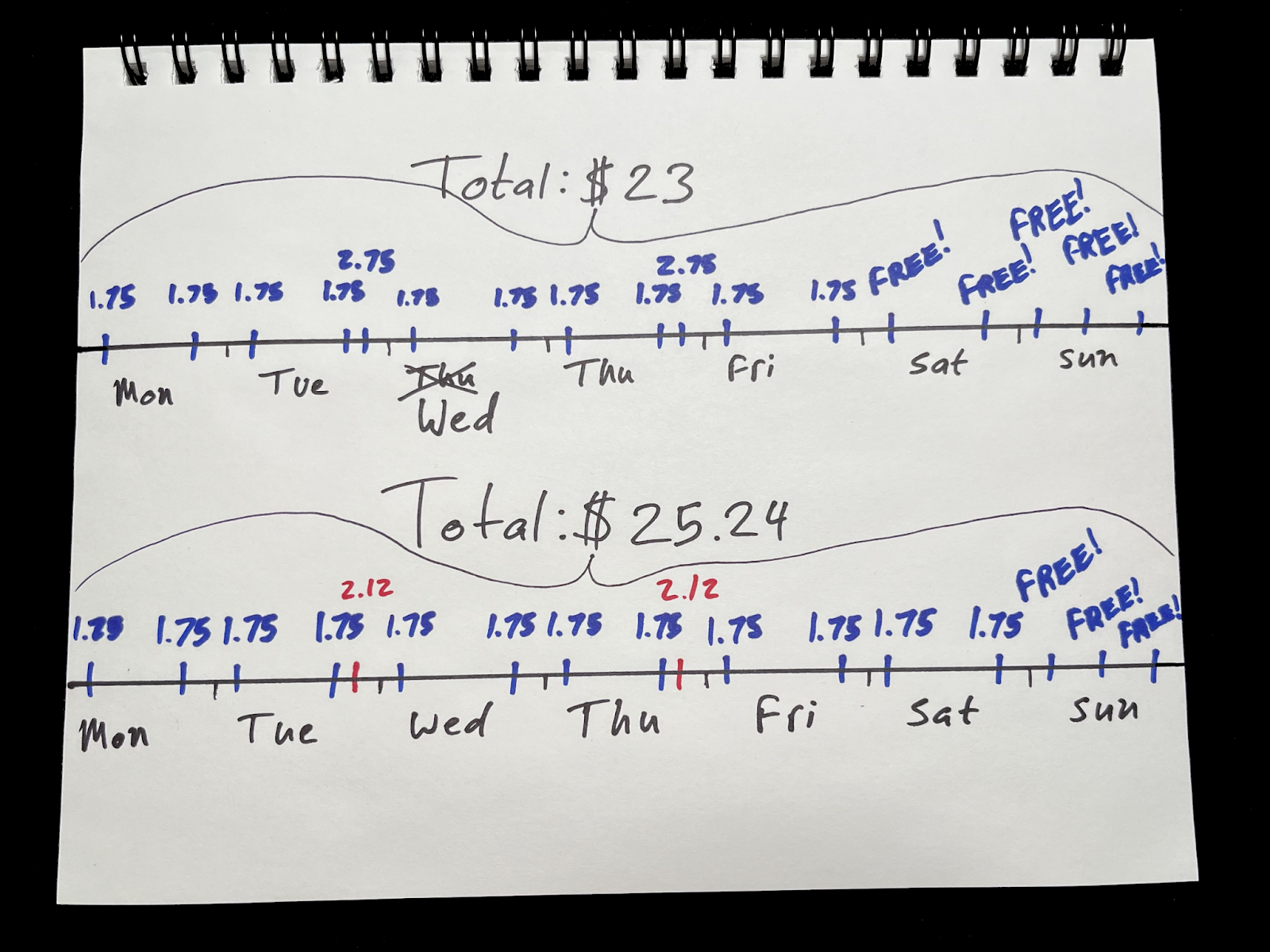

Here is an illustration of two weeks where our median New Yorker rides the subway seventeen times. In the top week, they use the Cash App card for every single ride, boosted or unboosted. In the bottom week, they use the Cash App card when the boost is available, and the Commuter Benefits card when the Cash App boost is not available. I hope the illustration makes it clear that, even though unboosted Cash App rides are more expensive than Commuter Benefits rides, using the Cash App card the whole time gets our commuter more free rides and lowers their total cost by the end of the week.

So, to recap:

The puzzle

We want to save as much money on the subway as possible, but there are three competing discounts. How do we use them all with maximum efficiency? The rules of the puzzle:

- The normal subway fare is $2.75

- The Cash App card lets you ride the subway for $1.75 every six hours (but if you need to use it more than once within six hours the additional rides are full price, $2.75)

- The Commuter Benefits card lets you ride the subway at a discount equal to your marginal tax rate

- When you ride the subway twelve times in one week with a given card, all future rides on that card are free

I have a solution to this puzzle, but it turns out writing takes a long fucking time (hence this post being three weeks late). In the interest of getting something out there, I’m going to leave my solution to this puzzle as a cliff-hanger for two weeks from now. Stay tuned! In the meantime, if you would like to think about the puzzle and send me your solutions, I’d love to see them!

Ta-ta now,

David